Regulations News

New Tax Policy Updates to Take Effect from January 1, 2026

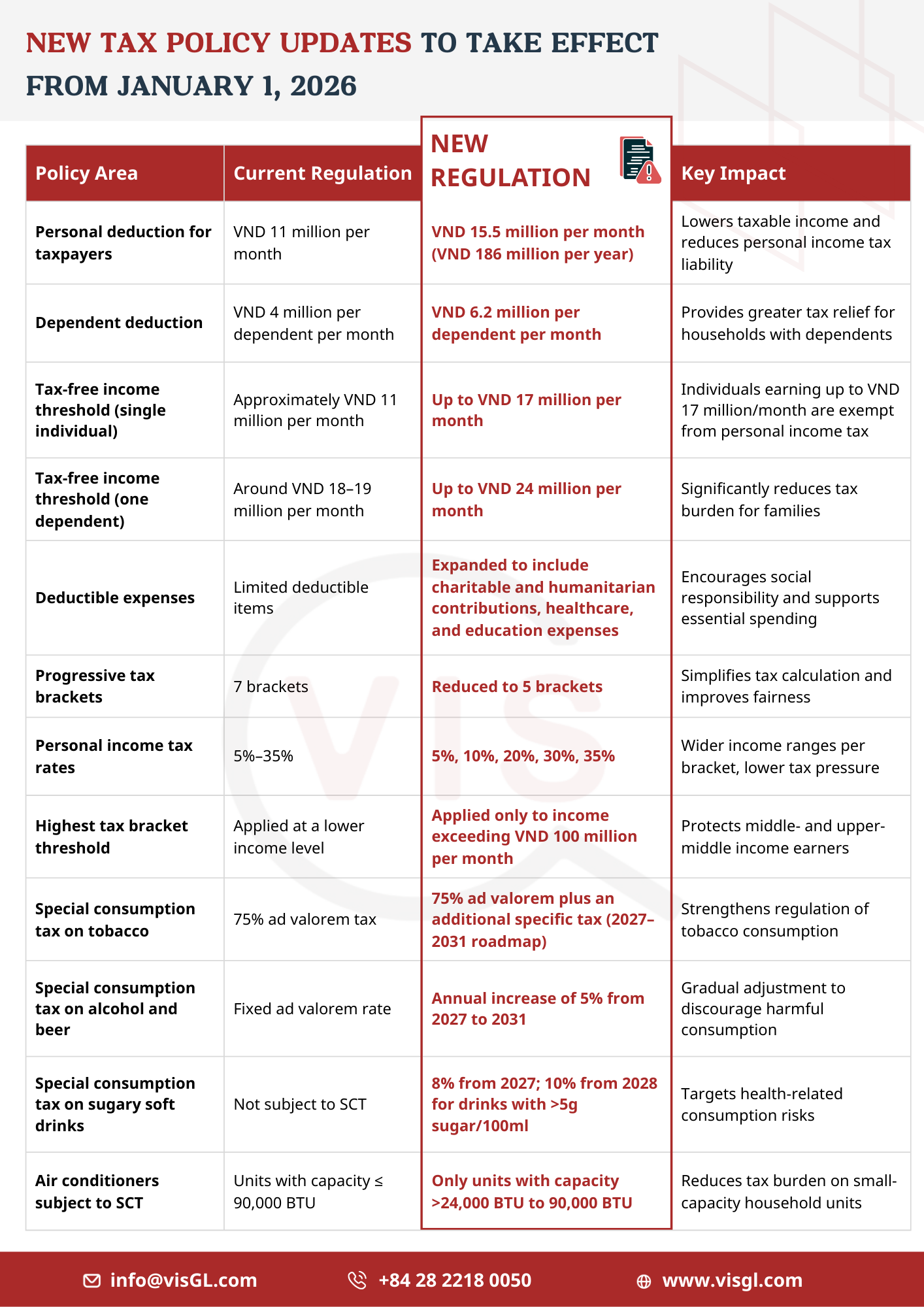

With the increase in personal and dependent deductions, millions of individuals are expected to see a reduction in personal income tax compared to current regulations.

Income of VND 17 million per month will no longer be subject to personal income tax

The amended Personal Income Tax Law will officially take effect from July 1, 2026. However, provisions related to income from business activities, salaries, and wages of resident individuals will be applied earlier, starting from the 2026 tax year, meaning January 1, 2026.

Under the new law, the deduction for taxpayers will increase from VND 11 million to VND 15.5 million per month, equivalent to VND 186 million per year. Meanwhile, the deduction for each dependent will rise from VND 4 million to VND 6.2 million per month.

With the revised family deduction levels, a single individual earning VND 17 million per month will not be required to pay personal income tax from next year (VND 15.5 million + VND 1.55 million = VND 17.05 million), resulting in a tax reduction of VND 210,000 per month compared to current regulations.

At the same time, each dependent qualifies for a VND 6.2 million per month deduction. This means that an individual with one dependent earning VND 24 million per month will not be subject to personal income tax, saving VND 610,000 per month compared to the current policy.

The amended law also expands deductible expenses, including charitable and humanitarian contributions, as well as healthcare and education expenditures for taxpayers and their dependents.

Progressive tax brackets reduced to five levels

Another notable change in the amended Personal Income Tax Law is the simplification of the progressive tax schedule, reducing it from seven brackets to five, while also widening the income ranges between brackets.

Accordingly, the applicable tax rates will be 5%, 10%, 20%, 30%, and 35%. The 5% rate applies to taxable income of up to VND 10 million per month, while the highest rate of 35% applies to income exceeding VND 100 million per month.

The new tax schedule is assessed to reduce tax obligations for all individuals currently paying taxes under existing brackets.

With the revised structure, all taxpayers subject to personal income tax will benefit from lower tax liabilities compared to the current system.

The new schedule also addresses abrupt increases between certain brackets, ensuring a more合理 and balanced progressive tax structure.

For the highest bracket (Bracket 5), the tax rate remains at 35%. The Government stated that this is a moderate rate, neither too high nor too low, when compared internationally and within the ASEAN region. Several neighboring countries such as Thailand, Indonesia, and the Philippines also apply a top marginal tax rate of 35%, while China applies a rate of 45%.

Increase in special consumption tax on alcohol and beer

The Special Consumption Tax Law 2025 will take effect from January 1, 2026, with policies aimed at regulating the consumption of products harmful to health, such as tobacco, beer, alcohol, and sugar-containing products.

For tobacco products, the law maintains the current ad valorem tax rate of 75% and introduces an additional specific tax under a five-year roadmap from 2027 to 2031.

For alcohol and beer, the law increases the ad valorem tax rate by 5% per year over a five-year period from 2027 to 2031.

For soft drinks meeting Vietnamese National Standards (TCVN) with sugar content exceeding 5g per 100ml, the tax rate will be 8% from 2027 and 10% from 2028.

Notably, under current regulations, all air conditioners with a capacity of 90,000 BTU or less are subject to special consumption tax.

However, from January 1, 2026, only air conditioners with a capacity above 24,000 BTU up to 90,000 BTU will fall under the scope of this tax.

Follow Vis Global Quality Control to stay updated with the latest Regulations News.